Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

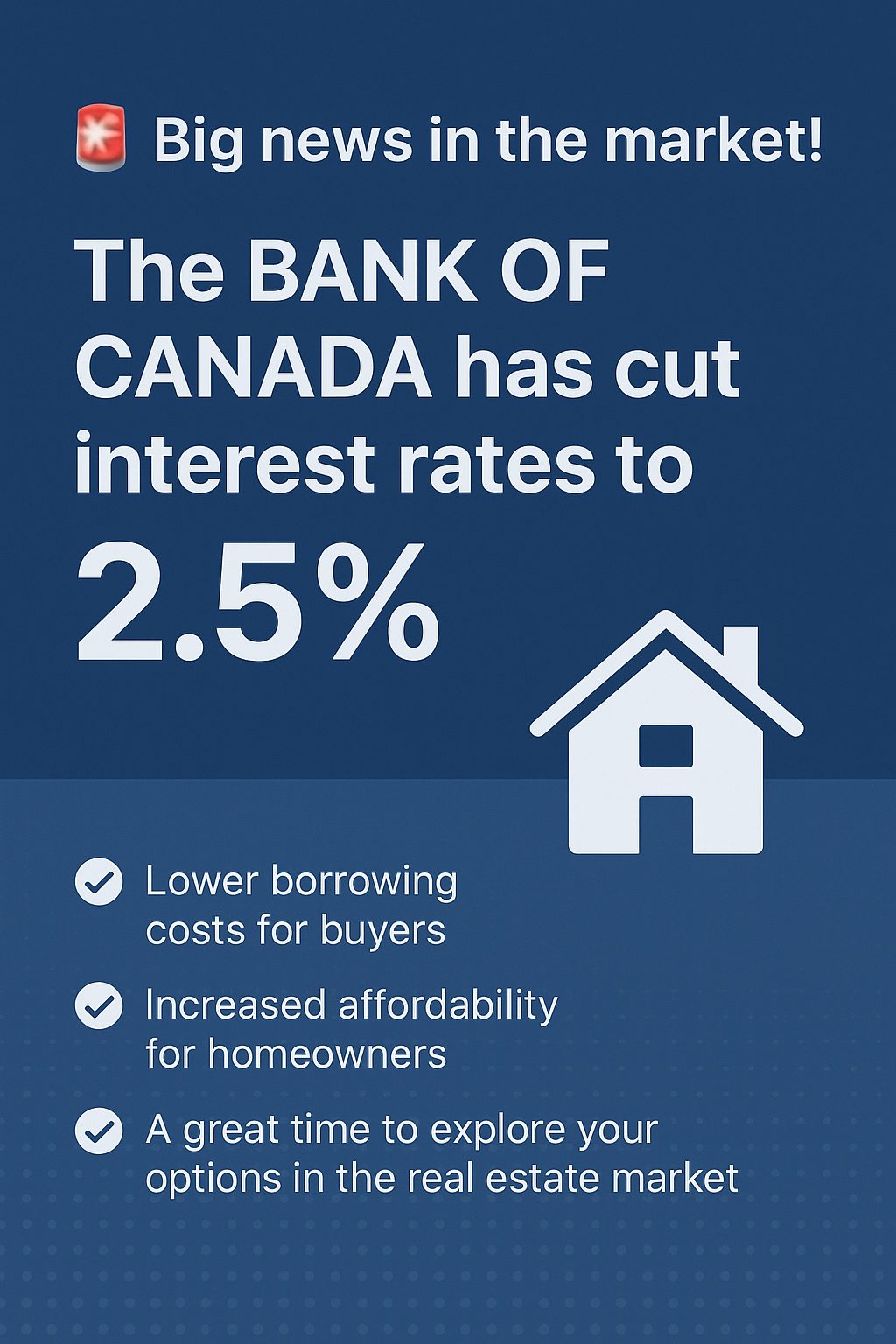

Today, the Bank of Canada announced a reduction in its policy interest rate (the overnight rate) by 25 basis points, bringing it down from 2.75% to 2.50%. This is the lowest the interest rate has been in about three years.

Why the Change

There are several key factors influencing the Bank of Canada’s decision:

-

Weakening Economic Activity: The Canadian economy contracted by around 1.6% in the second quarter of 2025.

-

Job Market Softening: Over 100,000 jobs reportedly lost in recent months. Unemployment has climbed to a high point not seen in many years (excluding unusual pandemic‐period distortions).

- Inflation Pressure Easing: While inflation remains above target in some measures, overall inflation (including core inflation) is showing signs of cooling. The Bank indicated that many inflationary pressures—especially those linked to trade and supply chains—are moderating.

- Global & Trade Uncertainty: Tariffs, international trade tensions, and external economic risks remain a concern.

What This Means for You

Here’s how this likely affects clients, depending on your situation:

| Situation | Likely Effect |

|---|---|

| Variable-rate loans / lines of credit | Lower interest costs. Monthly payments may decrease if your rate is directly tied to overnight or prime rates. |

| Fixed-rate mortgages / loans | No immediate change. Rates are locked in. However, new fixed-rate borrowing might become more affordable. |

| Savings, GICs, and short‐term investments | Returns may decline somewhat. If rates are lowered across the market, interest paid on savings products often follow. |

| Refinancing or mortgage renewal | You might get better rates if renewing or refinancing now, depending on lender policies and the fixed vs variable rate choices. |

What to Watch Going Forward

-

Core inflation metrics – The Bank will be monitoring whether inflation remains under control or pushes above target again. If inflation creeps up, rate cuts might stall.

- Economic recovery and labour market data – If the economy recovers more strongly, or unemployment drops, the Bank may pause further cuts. Conversely, continued weakness could lead to more easing.

- Global developments and trade risks – These have outsized effects since they influence both inflation (via import costs) and economic growth.

What You Can Do

If you are a client, here are some steps to consider now:

-

Review your variable-rate debt and project what savings you might see.

-

If you have fixed-rate commitments coming up, explore the market to see if refinancing makes sense.

-

Revisit your savings and investment strategy: lower yields may affect income from fixed income, GICs, etc.

-

Keep an eye on future rate announcements so you can anticipate further changes.